Summary

- Good returns over the last year, despite recent volatility

- Central Bank policy in focus

- Renewable energy – a positive (future) force in controlling inflation

- Octopus Money investment funds

Good returns from shares over the last year, despite recent volatility

Most investors have enjoyed good returns over the 12 months to end June 2026, despite no sign of an end to the war in Ukraine and a fragile ceasefire between the US and Iran. Globally, shares were up 28% (in GBP), despite geopolitical concerns and focusing more on strong earnings (85% of companies within the S&P 500 index beat Q1 expectations) and the opportunities of AI.

Markets have been a little choppy along the way, but as is often the way, those investors not reacting to market ups and downs were rewarded. There was a reasonable sell off in equity markets immediately after the attacks on Iran, but they rebounded strongly in April and May, whilst June was notable for a historic monthly fall in Microsoft shares, who suffered a 17% fall, as investors grew nervous about how highly some tech firms are valued, and how much they are spending to build AI infrastructure.

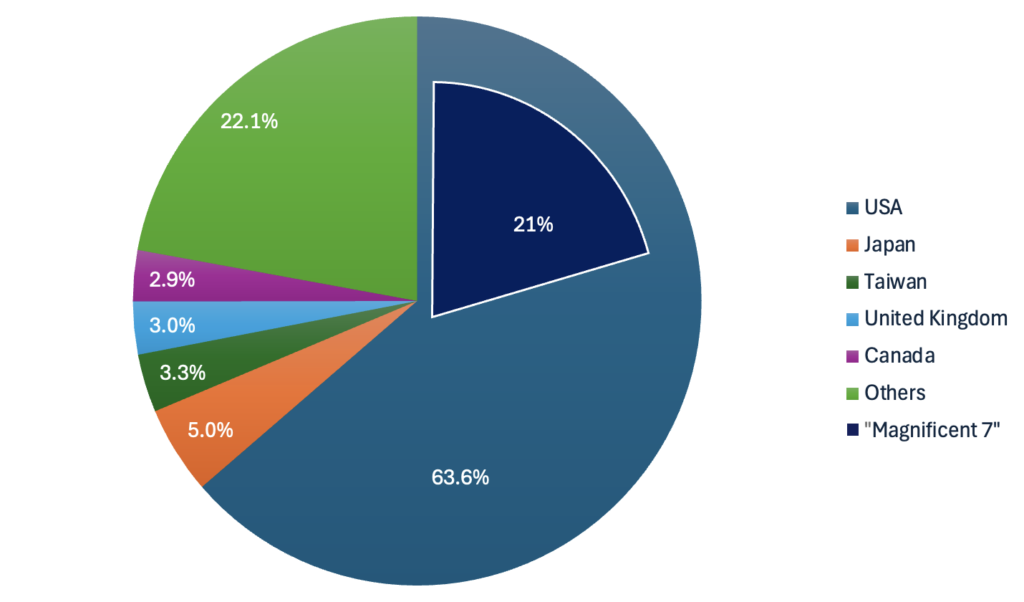

Regionally, the largest equity market, the US, was up 26% (in GBP) over the period with the S&P 500 Index reaching an all time high at the end of May. The US is home to most of the world’s largest tech firms (oftern referred to as the ‘Magnificent 7’), and valuations had been skyrocketing, before cooling in June as investors bet on who the AI winners are likely to be. Firms such as Amazon, Meta and Microsoft are investing huge amounts of money (forecast $700bn in 2026) in AI tech and supporting infrastructure.

This investment is spread across microprocessor designers and manufacturers (such as Nvidia and TSMC), the construction of huge datacentres, and driving multi-billion dollar contracts with renewable energy companies to power and cool them.

Global Market Sizes by Country vs “Magnificent 7”

Source (Lipper): MSCI All Countries World Index

But the massive demand on advanced processor chips has driven up prices, adversely impacting markets heavily reliant on chip imports, such as China. Chinese shares as measured by MSCI (a major stock market index provider) were down 2% (in GBP). China is the world leader in building out renewable energy infrastructure such as solar and wind power, as well as EV production, but they are heavily reliant on advanced chips being imported from Taiwan and Korea in particular.

However, whilst most share markets performed well over the period, bond markets were more subdued (global aggregate index up 3%), more heavily influenced by changing interest rate expectations caused by higher energy prices.

Central bank policy in focus

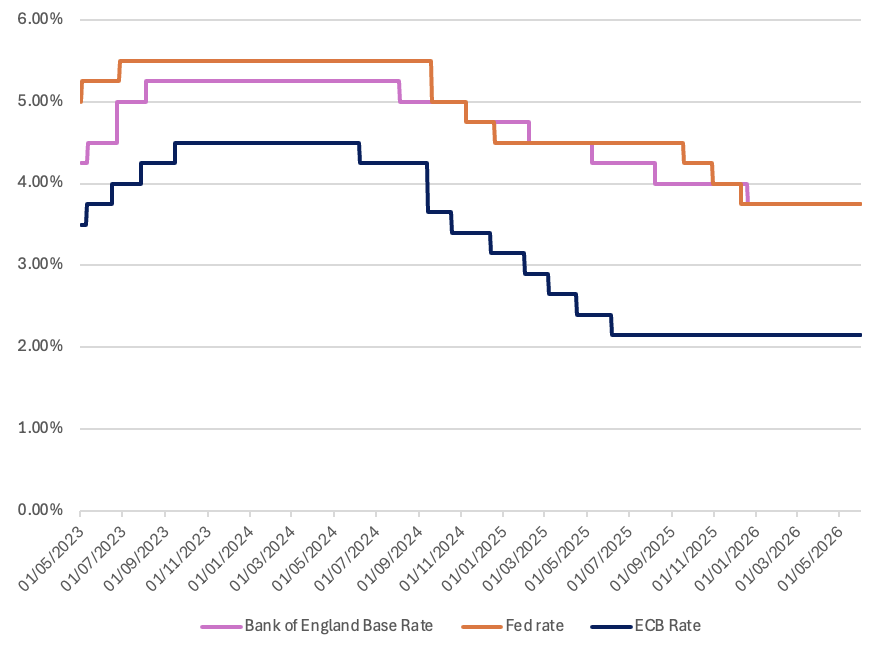

Markets started the year expecting further interest rate cuts, with inflation largely under control but economic growth being sluggish. This was positive for bond valuations through the latter stages of 2025. However, the attacks on Iran and the closure of the Strait of Hormuz saw energy prices spike, with Brent crude oil rising from below $60 to over $120, settling back to about $80 at the end of June. Inflation in the US has risen to 4.2% (above the 2% target) and with rising gas prices at the pump, the conflict with Iran is increasingly unpopular.

Instead of cutting interest rates to boost growth, the US Federal Reserve and the Bank of England have kept rates on hold so far in 2026, causing a re-pricing of bonds with the yield on ten-year Gilts (UK government bonds) rising above 5% for the first time in over a decade (although they did get very close to 5% during the Liz Truss ‘mini-budget in 2022).

There is a chance that the next move is upwards, but we think that unlikely. UK inflation was 2.8% for the 12m to end May, lower than expected, and forecast to peak around 3.3% by the end of the year. If inflation levels out at below 3.5%, and then starts to fall (as is predicted), we do not expect the BoE to raise rates, which should be positive for both shares and bonds.

Global Central Bank Interest Rates

Sources: Bank of England, European Central Bank, US Federal Reserve

Renewable energy, a positive (future) force in controlling inflation

Over the last 10 years, the UK has executed one of the fastest clean energy transformations in the developed world, effectively flipping its power grid upside down. A decade ago, in 2016, renewable energy accounted for less than 15% of the UK’s energy mix, but now accounts for nearly half of energy usage. The cost of adding new renewable energy sources is also much cheaper than it was, for example solar is now 85-90% cheaper than it was a decade ago due to tech advancements, manufacturing scale and shifting supply chains. Solar is now the cheapest form of new electricity generation for most of the world.

The lower reliance on fossil fuels across the world is good news on multiple fronts. It is better for the environment (lower Co2 emissions), more efficient (for example, an EV uses around 80% of its energy usage to move the EV, whilst a petrol car uses about a quarter, with most wasted in terms of unwanted heat generation), it can help lower costs and increase energy security.

However, to get the full benefit of the energy revolution, the UK needs to change its outdated system of linking prices to wholesale gas prices (which have risen due to the conflict in Ukraine and Iran). We also need to invest in grid and storage infrastructure to better accommodate the changes in energy supply. So whilst a 1970’s style oil crisis, hyperinflation, and 3-day working weeks are hopefully a thing of the past, there is still work to do to get the best out of the renewable energy revolution, with REMA (Review of Electricity Market Arrangements) expected to deliver positive change in 2027-28.

Octopus Money Direct investment funds

All Octopus Money Direct investment funds enjoyed positive returns for the 12-months to end June 2026. These ranged from 3.7% for the Bond Fund up to 29.3% for the Global Share Fund.

Octopus Growth Funds 1, 2, and 3

Starting with our three multi-asset growth funds; Growth Fund 1 (Cautious) returned 11.5%, Growth Fund 2 (Balanced) returned 20.2%, and Growth Fund 3 (Adventurous) returned 26.2%.. As the funds go up the risk-scale, more money is invested in shares, which outperformed bonds over the year.

Looking back over the last five years, returns from our three growth funds have on average been 3.4% per year, 6.9% per year, and 9.2% per year, with those investors willing to accept greater risk / fluctuations in value, rewarded, although of course past performance is not a guide to the future and there is no guarantee this pattern will be observed over the next five years.

The Defensive Fund – our lowest risk multi-asset fund – returned 7.9% for the 12-months to end June, a very good return for a fund which aims to keep risk low. The fund invests in a spread of assets blended to ensure volatility (ups and downs) remains low compared to our other funds.

The Bond Fund returned 3.7%, an ok result, but actually less than half of our Defensive Fund. By investing in a spread of assets, rather than just bonds, our Defensive Fund has approximately half of the volatility (ups and downs) of the Bond Fund, and can generate higher returns. We would encourage anyone investing in just the Bond Fund to consider our more diversified funds as likely better homes for their money – we would expect both Defensive and Cautious to generate better returns over the long term for less or similar risk.

The UK Index Tracker Fund was up 21.7%, a little behind the global average. Whilst some sectors performed very strongly, such as banks (+60%), mining (+79%) and healthcare (+33%), it hasn’t been plain sailing. Highlighting that not all are winners in the AI build out, RELX, the UK’s largest ‘tech’ company fell nearly 40% over concerns that some of its premium products (for example those that serve legal and medical practitioners) were losing relevance in relation to broader AI applications.

UK housebuilders such as Barratt Redrow and Taylor Wimpey (both losing close to a third of their value) have been hit by high mortgage rates cooling housing demand, plus build cost inflation. They also face a multi-billion pound lawsuit over collusion over higher prices for homebuyers, on top of £100m already paid in relation to sharing commercially sensitive information between themselves.

The Global Share Fund was the best performer, up 29.3%. The Fund has maintained a 10% underweight to the US (meaning it holds less in US shares than a typical global fund) in favour of Asia and Emerging Markets, and this has paid dividends with underlying funds aberdeen Evolve Asia-Pacific ex-Japan Fund up 51.8% and the iShares MSCI EM ESG Enhanced Fund up 53.5%.

These strong performers helped the Fund beat the average UK domiciled global equity fund by 10% over the period, a great result. Both of these Asian and EM funds are also prominent within Growth Funds 2 and 3, who also outperformed their peer group averages by about 6% each.

The Climate Change Fund generated a decent return over the last 12 months (11.8%), but this was notably behind global equities in aggregate (27.7%). Two of the largest holdings in the Fund are Microsoft and Taiwan Semiconductor Manufacturing Company, and their fortunes couldn’t have been more different, with TSMC more than doubling, whilst Microsoft lost a quarter of its value, having hit an all time high in October. Microsoft has been investing billions in AI, and TSMC have been one of the leading beneficiaries of that investment, operating at maximum capacity and aggressively raising prices on the chips they produce.

The fund has invested in Brazil for the first time, adding two new companies, Equatorial, a multi-asset utility company and Orizon, a waste management company. Closer to home, the fund’s investment in AstraZeneca worked well, with the shares rising close to 40% over the period, with impressive revenue growth and margins on its cancer treatments. AstraZeneca are held as a leader in terms of environmental practices within their industry, with ‘leaders’ making up just shy of 20% of the assets within the fund.

Visit each fund’s webpage if you want to see their returns over the last five years.

Remember, past performance is not a reliable guide to future performance.

Investment topics

Our experts dig a little deeper into the key trends and topics influencing investment performance.

Take a look at the performance of our funds

Investments

Check how your Stocks and Shares ISA or Investment Account funds have done.

Pension

Find out how your Pension funds have performed.